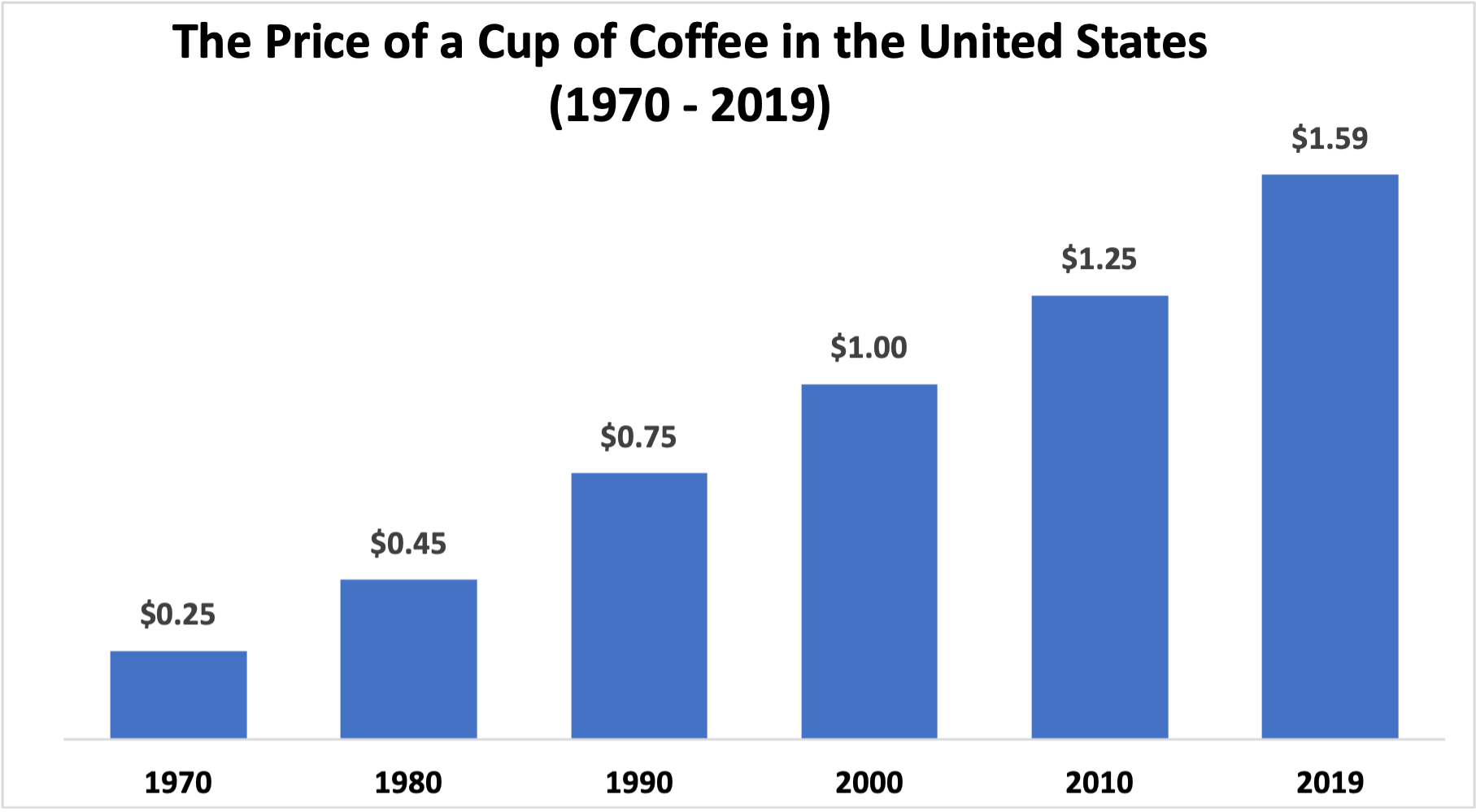

Inflation represents the change in purchasing power of a currency over time. When inflation is positive, the purchasing power of a currency declines. More units of that currency are required to purchase the same goods and services in future, in other words, prices appear to rise. Keeping track of how much of a currency is required to purchase the same goods over time measures the rate of inflation over time. The following chart shows the number of US dollars required to purchase a cup of coffee in the United States since 1970. Inflation over this period has not changed the value or quality of a cup of coffee, but it has increased the number of dollars you need to buy it. The value of the dollar when translated into a real asset has declined by close to 90% over this period.

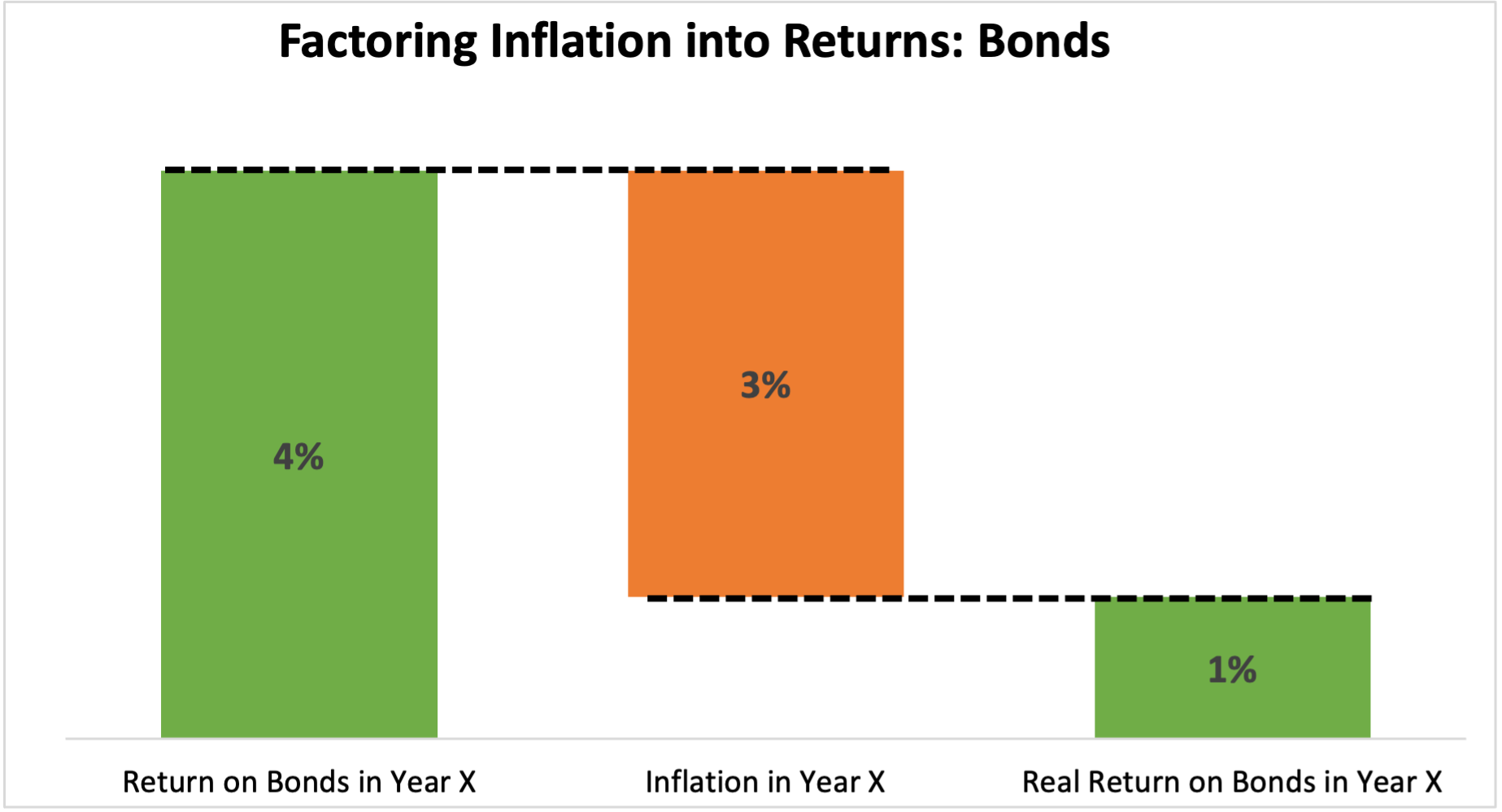

Inflation reduces the value of a currency over time. It is critical for investors to understand what this means for their investment returns. Imagine inflation in any year (Year X) is 3%. If the return on your investment assets in Year X is not at least 3%, your investment capital is worth less in real terms when translated into goods and services. The example in the following chart very simply shows this in relation to bond returns. We show returns from bonds in Year X of 4% (not bad), but then we factor in the effect of inflation which, remember, reduces the value of the currency. After this effect, the real return from bonds in our example is reduced dramatically to just 1%. Now imagine if the rate of inflation in Year X had been 5%, or 8%. Then our real returns turn heavily negative. Investors must seek investments with returns greater than the rate of inflation.

Investors in the developed world have enjoyed low, stable, and predictable inflation since the 1990s. This has allowed investors to focus on generating returns without having to worry too much about inflation as a risk. If inflation is 1% or 2% every year, this matters little to the real returns on bonds, equities or real estate which have been consistently strong for several decades.

This, however, may be about to change. The pandemic has shaken the global economy and resulted in dramatic changes to government and central bank policy. The US reported consumer inflation for April 2021 of +4.2%, the sharpest acceleration in prices in almost 15 years and close to the highest rates reported in decades. Inflationary fiscal and monetary policy, combined with pent-up demand and an economic recovery could see much higher rates of inflation in our near future. Investors must be prepared for this.

In any period of higher inflation, cash has been a poor performer. In a low interest rate environment, cash offers little protection to investors. It loses its value at the rate of inflation over time, with no mechanism to positively adjust in value. Bonds similarly have little capacity to adjust in price to reflect changes in inflation. Most bonds are fixed income instruments, this means the rate of return is fixed at a certain rate, say 5% per year. If inflation rises, as shown in the previous example, the real rate of return on fixed income assets declines.

‘If not bonds or cash, where then?’ many will ask, in relation to where capital should be allocated to weather any transitory inflation storm. ‘Equities with pricing power!’ is the emphatic response from the investment team at Dominion. Any business which has pricing power is able to pass on inflation in costs to its customers as price rises. These companies often have dominant positions in their markets, face little competition and sell unique products and services.

At Dominion, we invest only in companies that command pricing power and which are also growing profits at rates above GDP. We believe this combination of: (1) pricing power, and (2) growth, is a recipe for continued positive investment returns, whatever the inflationary environment may be in the coming years.