After the First World War and a global pandemic, the 1920s saw a decade of economic, cultural and artistic dynamism which transformed the world. Could the 2020s see a repeat of the Roaring Twenties?

The world is coming out of a major pandemic, after years of economic and political turmoil. The United States has just had a presidential election where the winner ran on a message of “returning to normalcy”, promising a new era of more stable politics and economic growth. The year... is 1920.

In the US election of 1920, Warren G. Harding ran for President with the campaign slogan: “Return to normalcy”. After the chaos of the First World War, followed by the human and economic tragedy of the 1918-1919 Spanish Influenza pandemic, a political message of stability and “normalcy” resonated with voters. The exhausted population of 1920 would be forgiven for having viewed their future as bleak. But what happened in the subsequent decade was remarkable in how different it was from the preceding decade of conflict and pandemic. The 1920s saw unprecedented technological development, economic growth in the developed world and a creative explosion that still influences modern culture today. Perhaps the 2020s, following a decade of political turmoil and a serious pandemic, could be about to surprise everyone.

Mark Twain is credited with having said: “History may not repeat itself. But it rhymes.”

Future historians may come to view the 1920s and the 2020s as decades when history rhymed. In the year 1920 and in the year 2020, investors found themselves in the midst of a pandemic ravaged economy where activity (both economic and cultural) had been suppressed, where consumers had ‘pent up demand’ from higher savings due to forgone spending during a pandemic, and where technological developments were set to transform the world around them over the coming decade. When we look at the investment outlook for our investment funds, we cannot help but be optimistic about the likelihood that the 2020s will be a decade of growth and transformation.

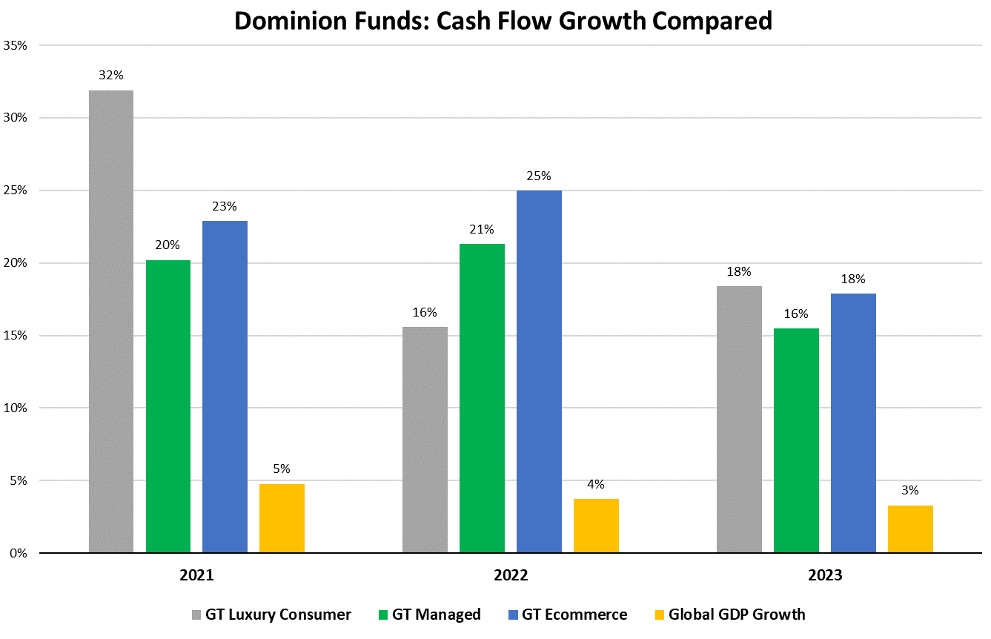

Looking at the outlook for Dominion’s investment funds, we see that the market agrees with our outlook for the 2020s. Expected cash flows in our fund investments are predicted to grow substantially in the first three years of the decade, well ahead of growth in the global economy (see below). This growth will be driven by the structural growth trends (Global Trends) we invest in across the portfolios.

We are optimistic about the future for the global economy, but we have even higher conviction that the 2020s will be remembered as the ‘Roaring Twenties’ for the structural growth trends we invest in through our Funds at Dominion. Following is a commentary from the Dominion investment team on the investment outlook for each of the Global Trends Funds.

Ecommerce Fund – A fantastic year in 2020 and exciting outlook ahead

The lockdown of much of the world in response to the COVID-19 pandemic has forced lasting behavioural changes. Foremost among these has been a migration of millions of new users to digital platforms. This has driven a major acceleration in the Ecommerce trend, with years of future adoption of digital platforms happening in just a few months in 2020. What is often under-appreciated about this incredible change is that the shift of our personal and economic lives onto digital platforms is irrevocable. This transformational change has generated +29.3% returns for the Fund in 2020.

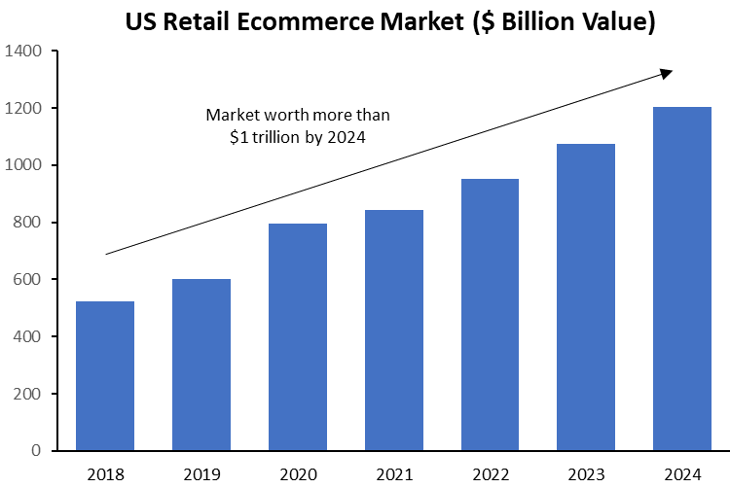

Growth of the digital economy, both in terms of its population and economic activity, does not stop when the COVID-19 pandemic is over. The gains of the Ecommerce businesses we invest in are permanent. US retail ecommerce sales, for example, are still forecast to grow by more than half over the next four years to more than $1 trillion.

The digital future for the developed world is happening now in China, the world’s largest ecommerce market at over $2 trillion in value. The Chinese ecommerce market is set to more than double in size by 2023, with ecommerce penetration moving above 60% of total retail. The question is not whether the rest of the world will look like China, but how quickly it will catch up.

The Ecommerce Fund, as a thought leader in the space, is well positioned to take advantage of this future growth. The average investment in the portfolio is predicted to grow its cash profits by +23% in 2021, followed by +25% and +18% in 2022 and 2023 respectively. The portfolio has positioned itself to also benefit from the ‘COVID recovery’, with one-fifth of the portfolio benefiting disproportionally from a resumption of more normal activities in 2021, while still benefiting from the long-term growth driven by the Ecommerce megatrend.

Managed Fund – COVID recovery and long-term growth themes will drive returns in 2021

The pandemic changed the world in 2020 and the Managed Fund adapted quickly to this new normal. We acted before the market crash in February to remove investment exposure to any sector impacted by the pandemic. This meant reducing or removing exposure to sectors like live music entertainment and sports events, travel booking and air travel. This action limited the downside to the Fund’s performance and gave us the ammunition to reinvest in businesses that continued to grow through 2020, with our investments in sectors like internet cloud and digital advertising performing very well. We have also increased our exposure to high quality ‘recovery’ names in sectors hard hit by the pandemic. These investments are already generating strong returns for the Fund after the vaccine announcements and we expect them to be big contributors to performance in 2021. The Fund has generated +18.3% returns in 2020 so far.

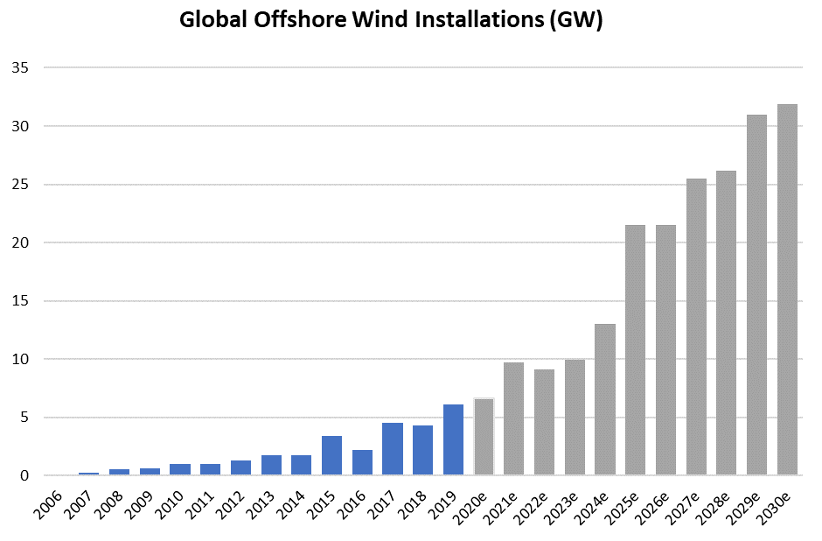

The long-term drivers of our Fund performance are still powering ahead, despite the pandemic. Our investments in long- term trends like electric vehicles and new healthcare technologies, for example, have continued to perform very well in 2020. The trends we invest in are fundamental, this means they are changing the world permanently, which gives us high confidence they will continue to drive strong growth in returns. Climate change is another example. In 2020 we increased our exposure to this trend with a new investment in the renewables and offshore wind sector, a critical part of the solution to climate change and a market expected to grow +600% by 2030 (see below).

Going into 2021 and beyond, the Managed Fund is well positioned for the short-term cyclical recovery from COVID, as well as being well placed for the continued growth upside from global megatrends.

Luxury Consumer Fund – Prospects look good for a strong recovery in 2021

In 2020, the pandemic posed a unique challenge to the companies serving luxury consumers, especially those relying on physical visitation. Good risk management by the investment team saw the Luxury Consumer Fund overcome COVID’s challenges and achieve positive returns. The Fund has generated +13.7% returns in 2020.

What the pandemic did not do was eliminate the underlying growth drivers of demographics, ageing, inequality, generational, social and technological change, which are core to our strategy. During the year some of these growth drivers were eclipsed (mobility, travel, leisure & tourism) while others shone more brightly (online shopping, private education and entertainment). Some consumer habits have changed because of social distancing but our portfolio companies have adapted. Some are even leading the change. The prospect of at least three viable vaccines may see those sectors that were weaker in 2020 shine once more in 2021 and beyond, adding further impetus to the Fund’s recent performance.

The Fund portfolio is undoubtedly well positioned for a dramatic reacceleration in growth. The average investment in the portfolio is predicted to grow its cash profits by +32% in 2021, followed by +16% and +18% in 2022 and 2023 respectively.

A bounce back from a pandemic can be viewed as a tide carrying all with it, even cyclicals and weak brands or businesses. A big rotation currently underway into so called “value” stocks reflects this. However, the problem with tides is that they inevitably recede beaching unsustainable businesses. Our focus on sustainable growth and its compounding wealth effects avoids second guessing cycles. Asset turnover for the Fund in 2020 will thus likely remain low as we continue to focus on “best of peers”.

Consumer and social changes like online shopping and remote working accelerated by the pandemic add to the attraction of equities as an asset class too. The TINA (‘There Is No Alternative’ to equities) hypothesis is likely to remain valid throughout 2021 and the promised explosive growth momentum reflecting “pent up” luxury demand (already evident in China) plus “more normal” consumer behavior means the Luxury Consumer Fund will likely materially improve upon its recent performance.

In 2019, China accounted for a third of global luxury demand and generated more than 50% of new demand growth. We stuck with traditional luxury companies with large Asia demand exposure throughout 2020. First into COVID, China was also first out and the one-party-state has since coped better in normalizing consumer life while averting second & third waves. Asia exposed companies’ sales are now mostly back in positive territory, helped by pent up mainland China demand which has been amplified by draconian inbound quarantine restrictions which have deterred the world’s biggest source of travelling luxury consumers from departing their homeland. A new administration in Washington and an increasingly assertive administration in Beijing thus create both an opportunity but also a risk that is difficult to assess until Biden is installed in the White House. What is likely is that the rhetoric is likely to be less antagonistic than Trump’s!